Chapter 1: Basic Concepts of Indian Income Tax

Introduction

As we know that taxation law in India are very complex especially Income tax law and As a person from non finance background it is not easy to understand entire income tax word by word. So FinTax Literacy try to understand the easy understanding of income tax laws for an individual. So lets start

In india Taxation laws are divided into two section:

- Direct Tax (i.e Income Tax & Tax on undisclosed foreign income and assets)

- Indirect Tax (i.e GST, Custom Duty, etc)

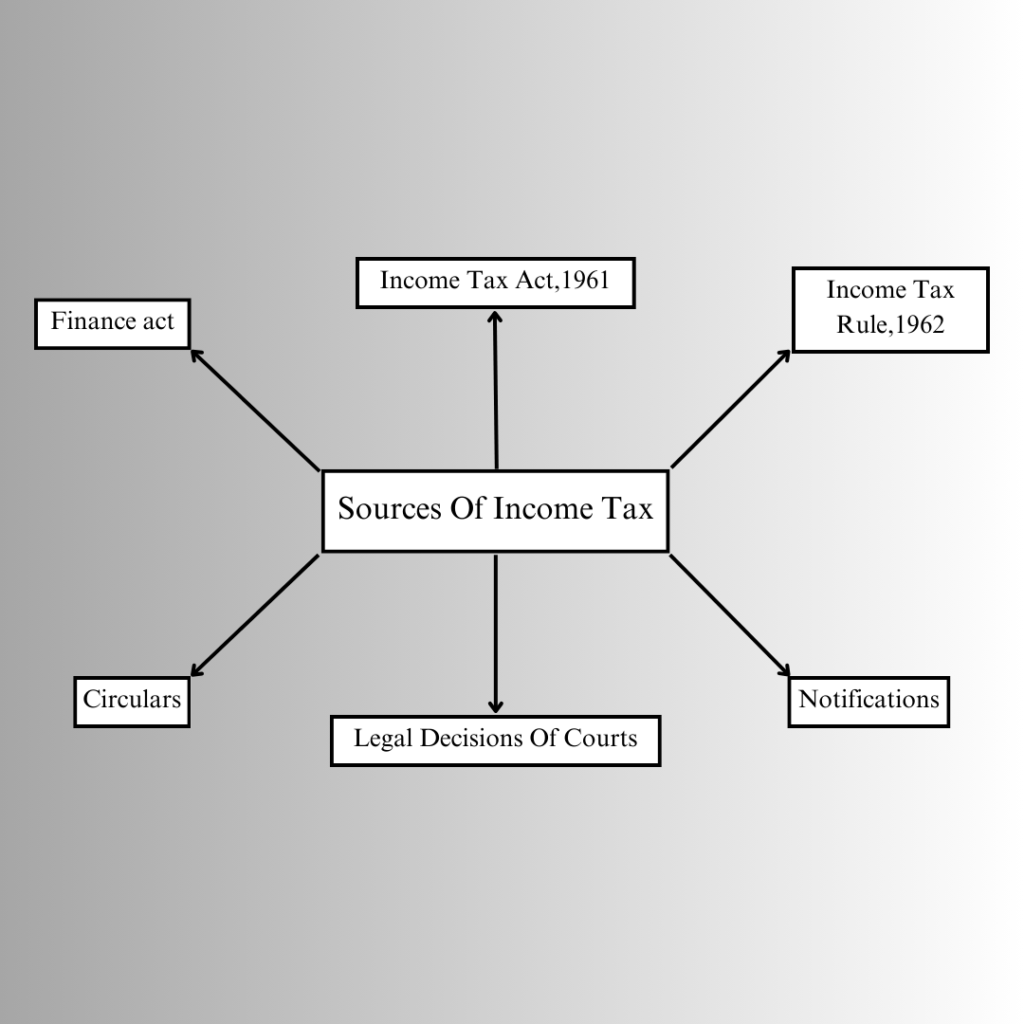

Sources of Income Tax Laws

- Income Tax Act, 1961:- The levy of income-tax in India is governed by the Income-tax Act, 1961. In the entire blog, we shall briefly refer to this as the Act.

- Income Tax Rule, 1962:– The Central Board of Direct Tax(CBDT) has empowered to make rules for carrying out the purposes of the above Act. So it is very important that these rules should also be study along with Act

- Finance Act:- Every year, the Finance Minister of the Government of India introduces the Finance Bill in the Parliament’s Budget Session. When the Finance Bill is passed by both the houses of the Parliament and gets the assent of the President, it becomes the Finance Act. Amendments are made every year to the Income-tax Act, 1961 and other tax laws by the Finance Act

The First Schedule to the Finance Act contains four parts which specify the rates of tax –

- Part I of the First Schedule to the Finance Act specifies the rates of tax applicable for the current Assessment Year. Accordingly, Part I of the First Schedule to the Finance (No. 2) Act, 2024 specifies the rates of tax for F.Y. 2023-24.

- Part II specifies the rates at which tax is deductible at source for the current Financial Year. Accordingly, Part II of the First Schedule to the Finance Act, 2024 specifies the rates at which tax is deductible at source for F.Y. 2024-25

- Part III gives the rates for calculating income-tax for deducting tax from income chargeable under the head “Salaries” and computation of advance tax for F.Y. 2024-25 where the assessee exercises the option to shift out of the default tax regime provided under section 115BAC(1A).

- Part IV gives the rules for computing net agricultural income.

- Circulars & Notifications

Circulars

- Circulars are issued by the CBDT from time to time to deal with certain specific problems and to clarify doubts regarding the scope and meaning of certain provisions of the Act.

- Circulars are issued for the guidance of the officers

and/or assessees.

- The department is bound by the circulars. While such circulars are not binding on the assessees, they can take advantage of beneficial circulars.

Notifications

Notifications are issued by the Central Government to give effect to the provisions of the Act. The CBDT is also empowered to make and amend rules for the purposes of the Act by issue of notifications which are building on both department and assessees

- Legal Decisions of Courts

- Case Laws refer to decision given by courts. The study of case laws is an important and unavoidable part of the study of Income-tax law. It is not possible for Parliament to conceive and provide for all possible issues that may arise in the implementation of any Act. Hence the judiciary will hear the disputes between the assessees and the department and give decisions on various issues.

- The Supreme Court is the Apex Court of the Country and the law laid down by the Supreme Court is the law of the land. The decisions given by various High Courts will apply in the respective states in which such High Courts have jurisdiction.

Assessment year v/s Previous Year

- Assessment Year(AY):- AY is the year (From 1st April to 31st March) in which persons are required to pay tax and file ITR(Income Tax Return).

- Previous Year(PY):- PY is the year (From 1st April to 31st March) in which persons earn or received income from various sources or in which TDS has on such income.

For Example, Mr A a salaried individual received monthly salary of Rs. 1,00,000/- in April 2024 to Mar 2025.

So Mr A earned income in Financial year 2024-25 so it is called Previous Year and requied to file ITR and pay Tax in Financial Year 2025-26 so it is called Assessment Year.

General Rule:

- Income of Previous year (PY) is Taxable in Assessment Year(AY)

- Exception to General Rule: Cases where income of PY is Taxable in PY itself

- Income of Non-Resident shipping business

- Income of Person leaves India permanently or for long duration.

- Income of discontinued business.

- Income of person trying to transfer his assets for avoiding tax.

- AOP/BOI/AJP formed for particular purpose

Person v/s Assessee

Person:- Person include the following

- Individual: such as Man Women

- Hindu Undivided Family(HUF)

- Firm: Such asPartnership Firm or Limited Liability Partnership

- Company

- AOP/BOI (Association of Person or Body of Individual)

- Local Authority: Nagar Nigim, Muncipal Corporation

- Artificial Juridical Person: Courts, Temples, University etc

Assessee: Assessee means a person by whom any tax or any other sum of money is payable under this Act.

In other Word, Person included every person whether he is required to pay tax or not under this act but Assessee included only those person who required to pay tax under this act.

For Example There are two person, Mr A whose Annual Income of Rs. 12,00,000/- and Mr. B whose Annual Income of Rs. 2,40,000/- and As per Income Tax Act , Every person required to pay tax if his total Income exceed Basic Exemption Limit(i.e above of Rs. 2,50,000)

Therefore Mr A and Mr. B both comes under the definition of person but only Mr A comes under the definition of Assessee.

We hope you understand all the above concept if you have any doubt any of the above topic then you can asked from us on the info@fintaxliteracy.com email id. In the next chapter we will going to understand Computaion of total Income & Tax Liablity and Tax rates applicable of various Assessee under the Income Tax Act, 1961.

Happy Learning!!!

Disclaimer:

The contents of this document are for information purposes only. This aims to enable public to have a quick and an easy access to information and do not purport to be legal documents.

Viewers are advised to verify the content from Government Acts/Rules/Notifications etc.